Backing bars & restaurants

How VCs and family offices invest in retail ventures

“I’m one of the owners,” you shout over your shoulder to two friends following you through a packed West Village wine bar to your back table. “Sydney Sweeney sat here last night!”

The social flex of being a restaurant “owner” (i.e., writing a check into a friend’s-friend’s new restaurant or bar concept) is great for the ego, but often comes at the price of losing your investment.

Meanwhile, VCs and family offices see the same deals but tend to reach very different outcomes thanks to how they structure their investments.

Over the years, I’ve watched friends write checks ranging from fifty thousand to half a million dollars into hospitality ventures they didn’t structure properly—and lose most of it.

It rarely feels reckless when writing the check. You think you’re backing a passionate operator who’s partnered with “the best up-and-coming chef”… for a concept that’s been sorely missing in a highly-trafficked neighborhood… where they just signed a below-market lease on the perfect space.

On paper, everything works (I’ve never seen a business plan that doesn’t make money). In practice, very little goes according to plan.

After a few months, reality sets in:

Buildout overruns eat the opening cushion;

Rent escalates faster than revenue;

A key manager leaves with half the staff;

Food costs force changes to the menu and drive out regulars;

First distributions never materialize.

And before long, investors realize they funded a lifestyle business with venture risk, minimal upside, and no structural protection.

Next time you get a shiny deck for a new hospitality concept, follow the same structural playbook used by VCs and family offices when underwriting high-risk retail ventures:

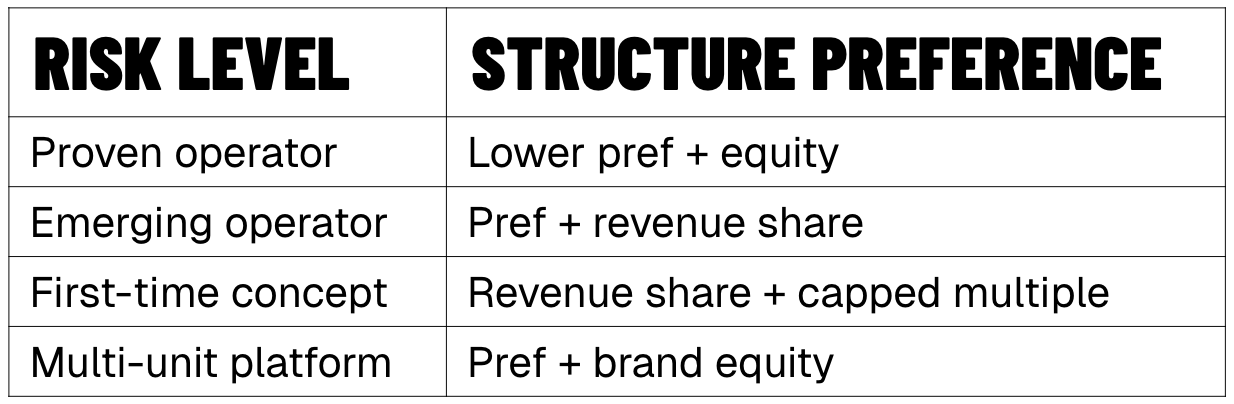

1. Structure capital to get paid early

Don’t rely solely on common equity appreciation in hospitality deals. The goal is to create cash flow visibility even if expansion never materializes or exit markets soften.

Hospitality is operationally volatile, margins are thin, and timelines to scale can be highly unpredictable—so investors need mechanisms that return capital early, not just upside at the end.

So alongside typical equity splits after investor payback (usually 70/30), build in:

Preferred returns of 6-10% (this comes out of operating cash flow before investor capital is returned); and/or

Gross revenue shares of 4-8% (usually capped at ~1.5X invested capital, then burns off or converts to common equity)

How to think about it:

A simple structuring question is to ask yourself: “How much of my capital is at risk after year two?” If the answer is “all of it,” you need to restructure.

By stabilization, some combination of partial payback, pref accrual, or revenue participation should already be underway.

2. Diligence the operator like a portfolio company CEO

You should spend far more time underwriting the people than the concept.

In hospitality, execution risk almost always outweighs concept risk. A strong operator can recover from a mediocre idea; a weak operator can destroy even a great one.

Ask the operator to talk you through their prior openings, historical unit economics, staff turnover, vendor relationships, and how prior investors fared.

Some things you should be listening for:

EBITDA margins of 15-25% for bars / fast casual, or 8-15% for full service

Prime costs (food + labor) below 60–65%

GM tenure of at least 3-5+ years and Chef tenure of at least 2-4+ years

Annual hourly staff turnover below 80%

Vendor payment terms on Net 30 vs COD

Stabilization within 12 months

Prior investors are reinvesting

If prior investors are not coming back into new locations, treat that as a meaningful signal—and ask why.

3. Underwrite the lease as aggressively as the concept

You should view the lease as one of the most consequential documents in the deal.

In many hospitality ventures, the lease—not the menu, brand, or buildout—is what ultimately determines whether the unit can generate durable margins.

Have the operator walk you through the terms, specifically looking out for:

Rent relative to projected revenue: 6-8% of gross revenue

Escalation schedules: 2-3%

Tenant improvement allowances: 20-40% of total costs

Guarantee structures: make sure investors aren’t exposed

So if projected annual revenue is $3mm, then:

Safe rent = $180K-$240K/year

Stretch rent = ~$300K

Risky rent = $400K+

Also, try to negotiate approval rights around lease amendments because occupancy cost drift can erode margins faster than most operational missteps.

Occupancy costs are one of the few line items that are both large and difficult to change once the business is open—which is why experienced investors treat lease structure as a primary underwriting variable rather than a secondary legal detail.

4. Negotiate investment into the TopCo

Long-term value in retail ventures rarely sits at the unit level. If the first location works, founders often open second and third units; launch franchise models; license the brand; or sell the platform to a larger hospitality group.

In most successful hospitality concepts, the enterprise value is created by the brand and the system, not the four walls of the first location.

So if you’re investing in Location #1, you should always negotiate exposure to the TopCo, BrandCo, or IP HoldCo that sits above the operating entities.

Practical ways to structure this include:

Equity in the parent entity that owns the brand and trademarks;

Pro-rata rights to invest in future locations;

Royalty participation tied to franchise or licensing revenue;

Conversion rights if multiple units roll up into a consolidated platform.

A general rule of thumb: 20% of TopCo should be allocated to equity investors in Concept #1, so you should receive your pro rata share of that 20% (e.g., if equity raise is $1mm and you invest $100k, you should own 2% of TopCo).

Without TopCo exposure, investors in the first unit often finance the brand’s proof of concept but capture little of the upside when the platform scales.

5. Build governance, even in minority positions

Even at 10-30% ownership, negotiate protective provisions that allow you to monitor performance and influence decisions that could impair investor economics (and if you don’t have +10% ownership; link arms with other investors).

In smaller hospitality deals, governance can feel informal—but that informality is what creates risk when performance deteriorates or capital needs change.

Typical governance rights include approval over:

New debt or credit facilities;

Admission of new partners;

Major capital expenditures;

Expansion pacing;

Lease renegotiations or relocations.

You should also require formal reporting expectations, specifically: monthly financial statements, KPI dashboards, and budget-to-actual reviews.

6. Plan for key-man risk before it materializes

Restaurants and bars are unusually dependent on a small number of individuals whose departure can materially impact performance. Underwrite this concentration risk early rather than reacting to it later.

Investors should protect themselves by putting structural safeguards in place that reduce dependence on any single operator, manager, or even chef. These protections often include:

Vesting schedules tied to operator equity;

Employment agreements with defined tenure expectations;

Non-compete and non-solicit provisions;

Retention incentives tied to performance milestones.

You should also think through contingency planning before it’s needed. That means determining who could step in operationally, how supplier and staff relationships would be preserved, and what financial reserves or credit capacity are available to absorb any disruption.

7. Define exit pathways at the outset

Many hospitality investments are made with no defined liquidity plan. Investors assume distributions will materialize or that someone will eventually buy the business, but those outcomes are far from guaranteed.

Professional retail investors approach hospitality the same way they approach early consumer brands. They map liquidity pathways before committing capital.

Common exit scenarios include:

Sale to a strategic hospitality operator;

Franchise recapitalization;

Roll-up into a multi-unit platform;

Investor buyback once the business stabilizes.

These scenarios get codified in the operating agreement through:

Tag-along and drag-along rights;

Buy-sell provisions;

Put options after defined holding periods;

Clear distribution waterfalls upon sale.

Even when the investment originates from a social relationship or local opportunity, institutional investors treat liquidity as a structural component rather than a hopeful outcome.

In practice, the difference between a good investment and one where capital gets trapped is often determined less by operating performance than by whether exit mechanics were defined early and documented clearly.