The $300 Hotel Room

The most dangerous price point in real estate

My friend Nadine Choe—who writes brilliantly about luxury hospitality in her newsletter The Stanza—said recently: 'Aspirational luxury will be the hardest hit segment in the cycle ahead.'

She wasn’t talking about Aman. Or Motel 6.

She was talking about the middle—the hotels, restaurants, and experiences that are too expensive for the masses and not exclusive enough for the people who don’t care about price. The $300-a-night hotel room at The W or a Thompson hotel. The $35 entrée at the "elevated" restaurant with Edison bulbs. These are in the kill zone.

The more I sat with it, the more I realized she wasn’t just describing hospitality. She was describing a structural shift that’s reshaping the entire built world.

The K-shaped economy (which we’ve written about before in the context of land, lifestyle towns, and who’s buying what) isn’t just an income distribution chart anymore… it’s an investment framework. And the framework says this: the middle is hollowing out across every real estate asset class. If you’re building, buying, or operating anything that targets the aspirational middle, you’re standing on the thinnest ice in the market.

Let me walk through what this looks like sector by sector.

Hospitality: The luxury end is booming. Aman can’t build resorts fast enough. Billionaires are paying Jeff Klein $1M a year for membership to San Vicente. At the other end, budget-flagged hotels—your Tru by Hiltons, your extended stays—are posting strong occupancy because they serve a need, not an aspiration. In between? The upper-midscale and “lifestyle” segments are the ones sweating. RevPAR growth is stalling. New supply is getting harder to finance. Soho House, which built its entire brand in the aspirational middle, is fighting for survival.

Residential: Build-to-rent communities targeting the broad middle class—workforce housing, suburban rentals, affordable senior living — are seeing record institutional capital inflows because the demand is structural and enormous. Ultra-luxury residential in supply-constrained markets (Aspen, Nantucket, Jackson Hole) is trading at record prices because the buyer pool is expanding faster than anyone expected. But the aspirational middle—the $600K-$900K new construction single-family home in a mid-tier suburb—is where builders are getting crushed. Rates have priced out the move-up buyer. The product sits.

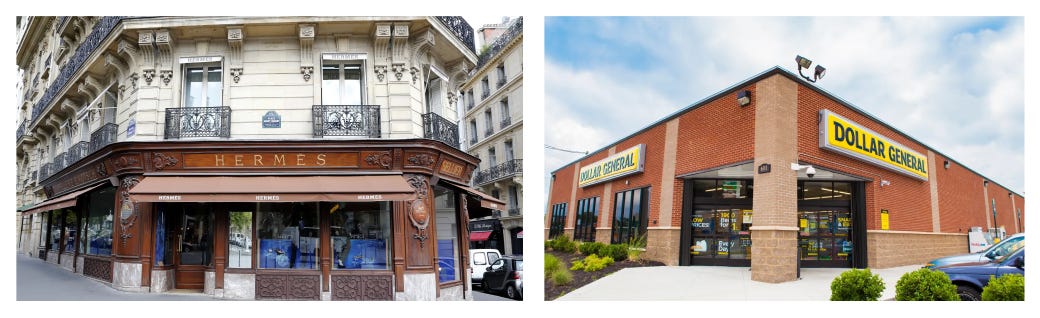

Retail: Dollar General opens 1,000+ stores a year. Hermès makes you spend $10,000 on scarves and jewelry just to get a 'leather appointment' (which is just a chance to be offered a handbag). Both are thriving. The retailers dying? The mid-tier department stores, like J. Crew and Pottery Barn, who sell “affordable luxury” and rely on a consumer who is stretching to afford something slightly above their station. That consumer is gone—squeezed by inflation, debt, and a labor market that rewards the top and automates the middle.

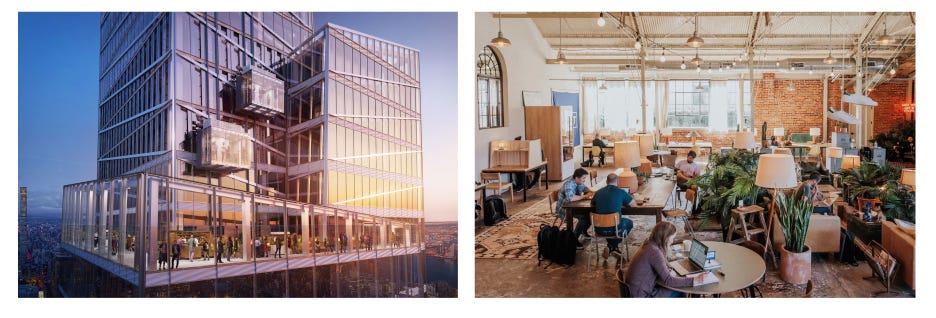

Office: Trophy towers in top CBDs are leasing. Companies want to bring people back, and they’re willing to pay for the best space to do it. At the other end, flex and coworking operators serving small businesses and freelancers are growing. Class B and C office—the “good enough” middle—is where vacancy rates are catastrophic and conversions (oftentimes to industrial, which no one would have believed 15 years ago) are the only viable path.

F&B: The $12 lunch and the $500 tasting menu are both working. The $45 entrée at the “elevated” restaurant with the reclaimed wood and the Edison bulbs? That’s the concept closing every month in every city I visit.

The pattern is the same everywhere:

The top is thriving because the ultra-wealthy are wealthier than ever and price-insensitive.

The bottom is thriving because necessity-driven demand doesn’t disappear.

The middle is collapsing because the consumer it was built for—the aspirational upper-middle class that stretched for nice things—is being economically squeezed out of existence.

For real estate investors and operators, the implication is uncomfortable but clear: you need to pick a side.

If you’re building for the masses, build for the masses… efficiency; cost per unit; and scale all matter. Don’t add the rooftop pool and the concierge package to a workforce housing project and call it “attainable luxury.” Just build good housing that people can afford.

If you’re building for the 1%, build for the 1%… create scarcity, experience and brand… these are the skills that will matter in these categories. The Harlan Estate model—tiny production, extreme quality, generational time horizon—works at the top because it refuses to dilute.

Nadine was spot on about hospitality. But the observation applies to every corner of the built world. The K-shaped economy isn’t a temporary dislocation but a new structure… and a framework for investing. And the built environment is going to conform to it whether we like it or not.

Build for the masses or build for the 1%. The $300 hotel room is a warning, not a strategy.

“The middle didn’t fail because of pricing. It failed because it lost its reason to exist.”

The $300 hotel room is exactly why STR operators in the right markets keep printing — guests get a full kitchen, living room, and washer/dryer for the same nightly rate or less. The value gap is obvious. Where operators get squeezed is in markets that are supply-saturated and competing purely on price. Market selection is everything.